Message from the Group CFO

Through disciplined practice of capital circulation management, we aim to achieve a state in which capital efficiency consistently exceeds the cost of capital by FY2026.

Managing Executive Officer Group Chief Financial Officer

Taisuke Nishimura

- Mid-term management plan: Achievements and challenges in the first year

- Mid-term management plan: Priority measures for the second year and beyond

- Fundamental approach to capital policy

- Realizing capital circulation management

- Key initiatives to realize capital circulation management

- Remittance operation based on free cash

- Business portfolio transformation

- Shareholder payouts

- Capital policy to achieve our Vision for FY2030

- Through dialogue with stakeholders to reduce volatility and strengthen our management foundation

Mid-term management plan: Achievements and challenges in the first year

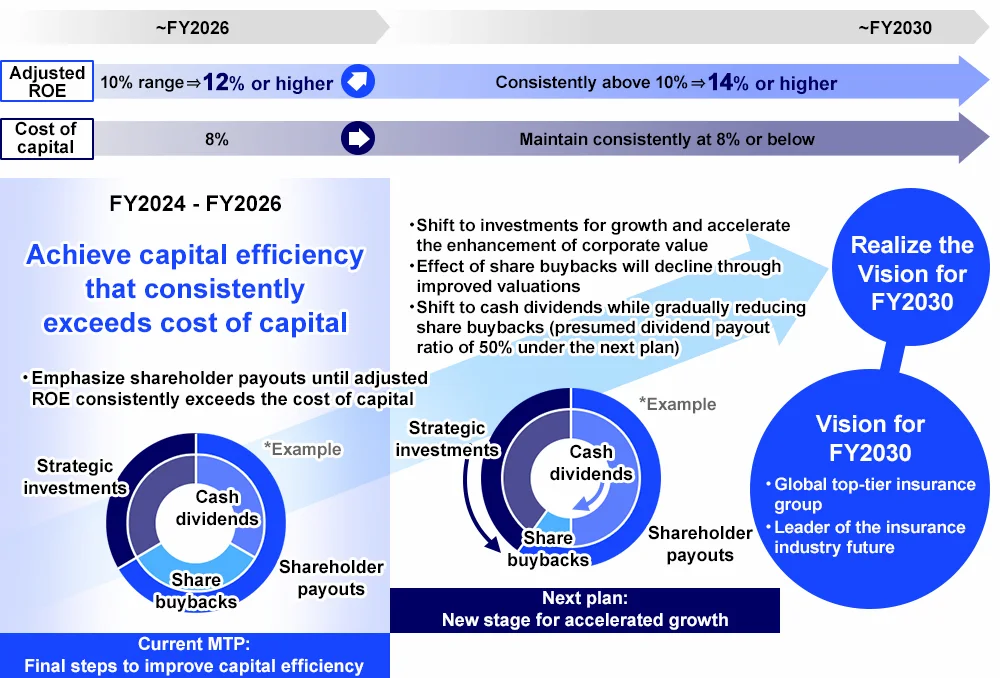

In the previous plan, we identified improving capital efficiency and lowering the cost of capital as the most important priorities and worked to reduce risk accordingly. As a result, by FY2023, the final year, we achieved certain progress, with the cost of capital declining to around 9%. At the same time, adjusted ROE, a key indicator of capital efficiency, stood at 8.2%, remaining below the cost of capital. Therefore, we positioned the current plan as the final stage toward achieving capital efficiency that consistently exceeds the cost of capital.

In FY2024, the economic environment remained stable at a high level, and Daiichi Life's new business performance recovered significantly. In line with its risk-reduction objectives, Daiichi Life made steady progress in selling domestic equities in accordance with the plan. Overseas subsidiaries, including Protective and TAL, also delivered solid results. As a result, Group adjusted profit reached ¥439.5bn, exceeding the ¥400bn target originally set for FY2026 when the plan was announced. Furthermore, through share buybacks and other initiatives to improve capital efficiency, adjusted ROE reached 10.7%, exceeding the 10% target set for FY2026, the final year of the plan, and for the first time our capital efficiency exceeded our cost of capital.

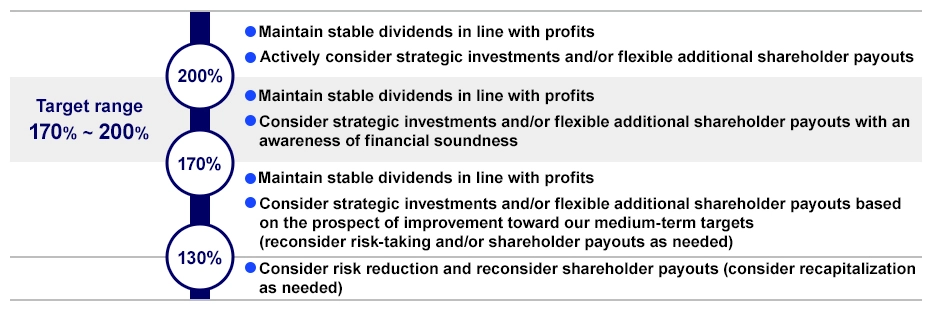

The Japanese government is scheduled to introduce economic value-based solvency margin regulations in FY2026. With this in mind, we have set an economic solvency ratio (ESR) target range of 170–200%. In addition to domestic subsidiaries that had already applied the standard in advance, overseas subsidiaries started adopting the new measurement model at the end of FY2024. In January 2025, we raised funds through a large-scale subordinated bond issuance, which pushed ESR above 200% and enabled investments in asset-formation initiatives and new businesses in the overseas life insurance domain. In addition, changes to the ESR measurement model brought the new standard-based ESR to 210% at FY2024 year-end, exceeding our target range.

With respect to improving operating expense efficiency—a challenge we have long recognized— changes in the economic environment, particularly the recent rise in inflation, now require stronger measures, and our management team is deepening discussions on concrete responses. We have already made proactive investments in such areas as IT and AI. Going forward, we aim to leverage the benefits of these investments to create further value and improve operating expense efficiency.

Mid-term management plan: Priority measures for the second year and beyond

From the second year of the plan onward, we need to further raise capital efficiency while maintaining financial soundness, thereby sustaining and expanding a position in which capital efficiency exceeds the cost of capital. With this in mind, we intend to drive capital circulation management even further.

As mentioned earlier, adjusted ROE in FY2024 reached 10.7%, exceeding our 10% target and reflecting progress toward achieving capital efficiency that consistently exceeds the cost of capital. It is important to note that this is not a temporary phenomenon, but rather a reflection of our intent to deliver consistently high capital efficiency in FY2025 and beyond.

While we achieved a high adjusted ROE, global top-tier peers we benchmark ourselves against are delivering even higher ROE levels. Therefore, we must also raise our sights and strive to achieve an even higher ROE. In light of these circumstances, we have raised our adjusted ROE target to 12% or higher for FY2026 and 14% or higher for FY2030. To achieve these targets, Daiichi Life sells its domestic equity holdings, with part of the proceeds to be reinvested in long-term JGBs. The capital released as profit will be allocated through the holding company to business investments that strengthen the competitiveness and profitability of Group companies. In addition, we will carry out disciplined and well-balanced capital allocation toward strategic investments for future growth and stable shareholder payouts as our most important priorities.

In Japan, a prolonged low interest rate environment has made it difficult for insurers to offer attractive assumed interest rate products, particularly in the asset-formation segment, but the recent rise in domestic interest rates has become a tailwind for the life insurance business. In the US, the world's largest insurance market where interest rates began rising ahead of Japan, the life and annuity market has undergone significant changes in recent years. The ability to manage assets in alternatives and securitized products has become a key success factor, and the asset management functions that support this have also grown substantially. As similar changes are anticipated in Japan, we are pursuing new product development that leverages the rise in yen interest rates with our efforts to strengthen our asset management capabilities. Through investments in the asset management field, meanwhile, we aim to achieve an average annual growth of 10% in adjusted earnings per share (EPS) from FY2023 through FY2030. To this end, we will support our business strategy to realize this growth from a capital policy perspective.

Since the start of FY2025, we have announced several strategic investments, but we also decided to withdraw from the Thai market. Looking ahead, we will continue pursuing strategic investments in businesses with high growth potential. If the initially expected benefits can no longer be realized, however, we will replace businesses in our portfolio. In this way, we will further advance capital circulation management by making disciplined and effective use of capital to drive growth.

We will continue striving relentlessly to enhance corporate value as we advance toward our Vision for FY2030.

Fundamental approach to capital policy

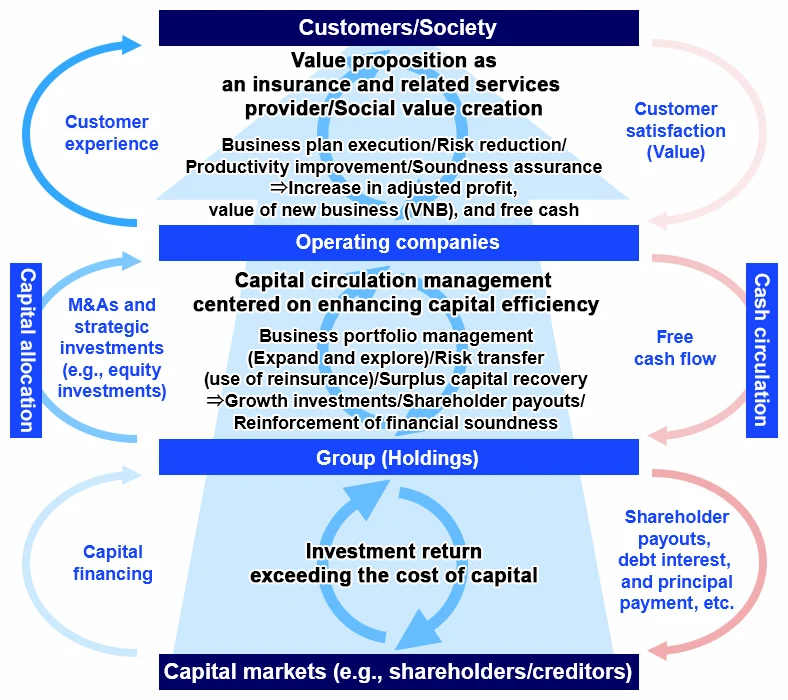

While maintaining financial soundness, the Group manages its capital policy based on the ERM framework, aiming for sustainable enhancement of corporate value and stable shareholder payouts.

Under our current mid-term plan, we will continue building on the previous plan by pursuing sustainable growth through the practice of capital circulation management. “Capital circulation management” means reallocating capital—sourced from earnings generated through business operations or freed up through risk reduction—to higher-efficiency, higher-growth businesses, while maintaining financial soundness. This creates a virtuous cycle of capital and cash generation that drives the enhancement of corporate value.

With respect to ESR, we have set a target range of 170–200%. When the level exceeds 200%, we will actively consider strategic investments together with agile and flexible additional shareholder payouts, taking into account market conditions and other factors.

ESR is an indicator of an insurer's financial soundness. Unlike the current solvency margin ratio, which is calculated using an accounting-based balance sheet, ESR is calculated using an economic value-based balance sheet.

Economic value refers to an evaluation that includes unrealized gains and losses on assets and liabilities that are off-balance-sheet under accounting standards. It enables consistent valuation of assets and liabilities using the same economic value basis and serves as an indicator that captures changes in the market value of liabilities arising from interest rate fluctuations— something not reflected in accounting information.

With respect to economic value-based evaluation, since our earlier mid-term management plan for FY2015–2017 we have disclosed a target ESR range of 170–200%. After introducing ESR, we have worked to enhance measurement methodologies, reflecting actual management conditions and responding to changes in capital regulations and other external factors.

At the end of FY2025, Japan is scheduled to introduce an economic value-based solvency regime (the “New Regulation”). This framework shares the specifications and basic structure of the International Capital Standard (ICS) applied to internationally active insurance groups (IAIGs) adopted by the International Association of Insurance Supervisors (IAIS).

In preparation for the New Regulation, we revised our calculation method for ESR at the end of FY2023 to align with the new standard for our three domestic insurers—Daiichi Life, Daiichi Frontier Life, and Daiichi Neo Life. At the end of FY2024, we also applied the new standard to our overseas insurance subsidiaries and changed the Group consolidation method accordingly.

Realizing capital circulation management

To advance capital circulation management, we are reducing market risk at Daiichi Life and tightening surplus capital management at subsidiaries. The surplus capital thus generated is being used for disciplined capital allocation to shareholder payouts including share buybacks, as well as strategic investments for future growth, aimed at improving capital efficiency. By generating stable cash flows from mature markets, particularly Japan, and continually allocating capital to growth markets with higher expected potential, we will drive sustainable growth for the future. In addition, through reinsurance and other intragroup financing mechanisms, we will further advance capital circulation management by optimizing the use of capital and retaining profits that had previously flowed outside the Group.

Key initiatives to realize capital circulation management

Risk reduction initiatives

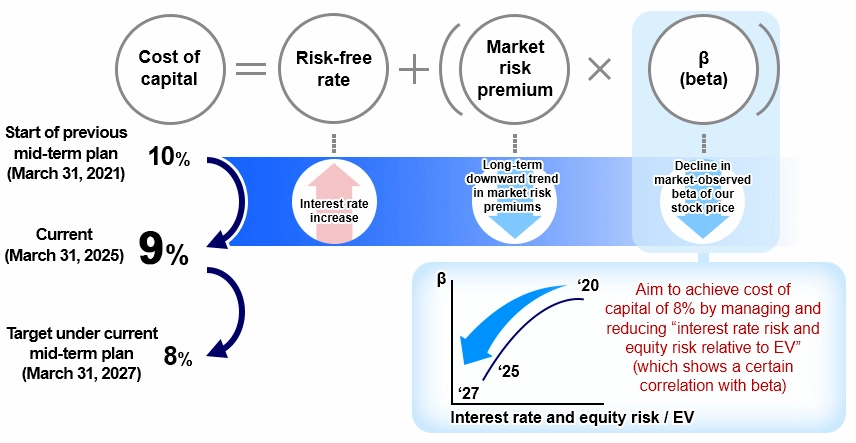

At the start of its current mid-term management plan, the Group's cost of capital we recognized was 9%. While closely monitoring the impact of rising interest rates in Japan and overseas on the cost of capital, we aim to reduce it to 8% during the current plan period through ongoing measures, such as interest rate risk and equity risk reduction.

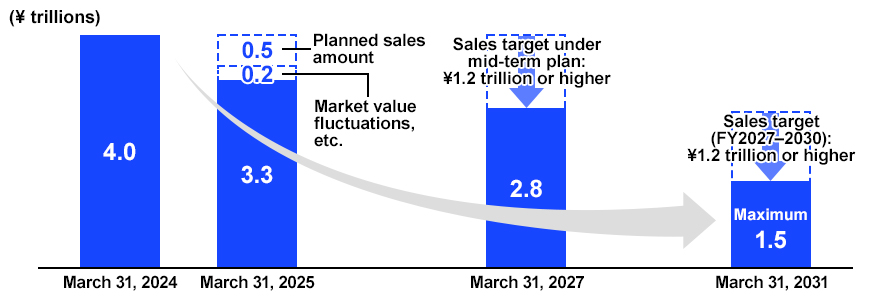

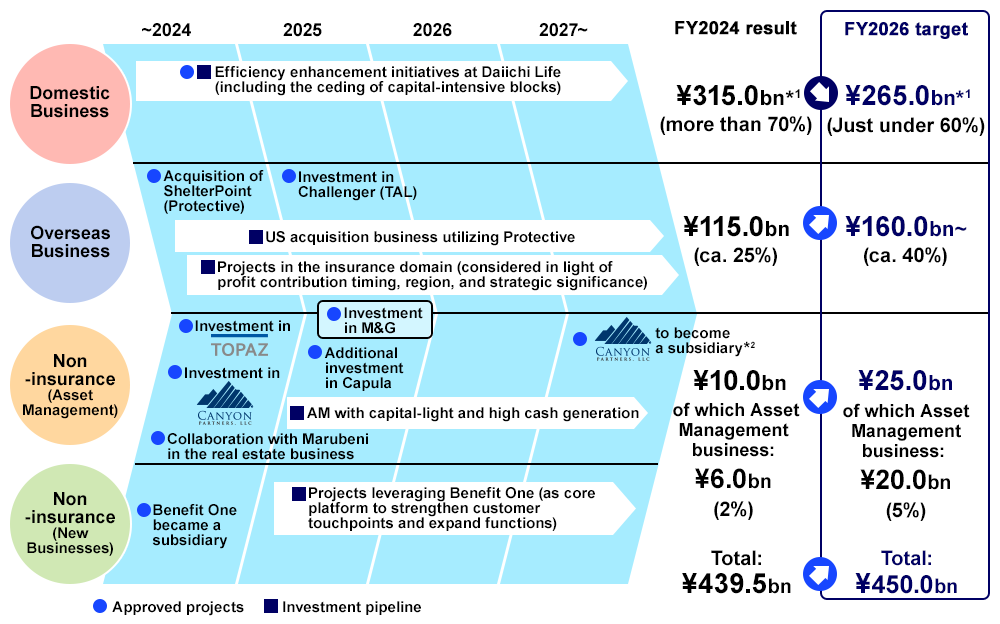

In FY2024, Daiichi Life reduced its market risk (sum of interest rate risk and equity risk) by ¥225.0bn year on year. Of this amount, we completed approximately ¥500bn in sales of domestic equities, representing a progress rate of 40%—earlier than called for under the plan—against the plan's cumulative target of ¥1.2tn. We will continue advancing this initiative in FY2025 and beyond to ensure that the balance of domestic equities is reduced to a maximum of ¥1.5tn by the end of FY2030.

Taking advantage of the New Regulation's introduction at the end of FY2025, we will move beyond simple risk reduction and work to upgrade our capital circulation management. This will include shifting toward risk portfolios that can deliver higher capital efficiency and thereby enhance corporate value.

Utilization of reinsurance

Under our capital circulation management policy, we have been making greater use of intragroup reinsurance in recent years. Since establishing our reinsurance subsidiary, Daiichi Life Reinsurance Bermuda, in 2020, Daiichi Frontier Life, Daiichi Neo Life, and TAL have utilized intragroup reinsurance for purposes aligned with their respective business characteristics. Group companies are also using external reinsurance to shift risks and free up surplus capital. For example, Protective made a large-scale transfer of a block of in-force policies worth around ¥1tn. We will continue promoting capital circulation management by using reinsurance and other measures to make effective use of capital.

Remittance operation based on free cash

The amount of dividends remitted from operating subsidiaries to the holding company is determined based on “free cash,” or distributable capital, which takes into account the ESR range as well as solvency regulations and accounting constraints in each country. In FY2024, the amount of such dividends equated to a remittance ratio of approximately 86% of Group adjusted profit, mainly because Daiichi Life's profit level exceeded the initial projection. For FY2025, we forecast Group adjusted profit of around ¥410.0bn. Assuming a remittance ratio of roughly 90%, we estimate that free cash will amount to around ¥360.0bn.

| Remittance amount | |

|---|---|

| Daiichi Life | ¥287.1bn |

| Protective*1・3 | ¥27.3bn |

| TAL*2・3 | ¥49.8bn |

| Group | ca. ¥375.8bn |

- *1Remittances from Protective and other overseas subsidiaries are, like those from domestic subsidiaries, partly reclassified as being received by the holding company in the following fiscal year

- *2Dividends on FY2024 profit retained in connection with the investment in Challenger

- *3Based on the exchange rate as of March 31, 2025

Business portfolio transformation

We are working to reinforce our core businesses—protection and asset formation/succession—while exploring new areas, such as digital, health, and medical services, with the aim of optimizing our business portfolio through continuous expansion and diversification.

Through Protective, we acquired ShelterPoint, which operates a group insurance business in the US, in FY2024. Since the start of FY2025, we made an additional investment in Capula, a leading hedge fund in the UK. We also decided to invest in Challenger, the leading company in Australia's individual annuity market, through TAL. In addition, we resolved to invest in UK-based M&G, a major player in the asset management and life insurance fields in Europe. To optimize our business portfolio, we divested our Thai business, Ocean Life, as its strategic importance declined due to slowing market growth and other factors.

Seeking to achieve our profit target of ¥450.0bn in FY2026, we will carefully select investment opportunities while aiming for a well-diversified and efficient business portfolio—balanced across risks and regions—and disciplined capital allocation.

- *1Includes the Company's amortization and related costs

- *2We hold an option to acquire a 51% majority stake (unexercised as of May 31, 2025)

Shareholder payouts

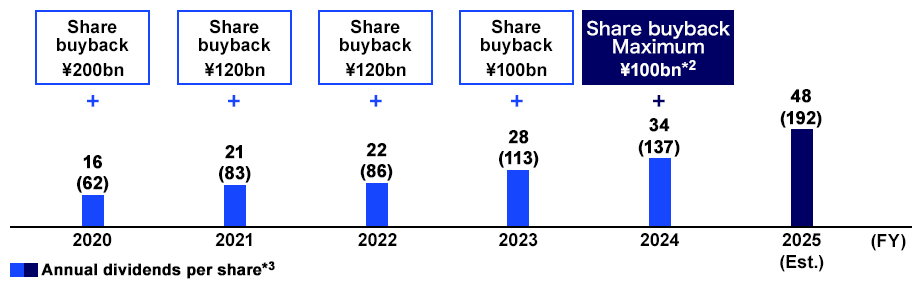

For shareholder payouts in FY2024, we paid a year-end cash dividend of ¥76 per share. Together with the interim dividend, this brought annual cash dividend to ¥137 per share, up ¥24 from the previous year. In addition, we launched a share buyback program in May 2025, with an upper limit of ¥100.0bn, marking our fifth consecutive year of large-scale share buybacks.

Starting in FY2025, we will raise our dividend payout ratio from the previous 40% or higher to 45% or higher. At the same time, we set a medium-term average target for total payout ratio at 50%. Considering various factors, such as ESR, cash flow, growth investment opportunities, and our share price, we are strategically considering and implementing agile, flexible additional payouts through share buybacks.

We aim to further enhance shareholder payouts by driving sustainable growth in Group profit and strengthening our capacity to generate capital and cash.

![Stable dividends in line with profit [Dividend payout ratio] 45% or more each year ・ In principle, we will not reduce the annual dividend per share ・ In principle, we pay an interim dividend / Consideration of agile and flexible additional shareholder returns ・ The scale, timing and other factors are determined strategically ・ Guideline for total payout ratio: mid-term average of 50%](/en/investor/img/message_im09.webp)

- *1The dividend payout ratio has been raised to 45% in FY2025 to ensure a stable shareholder payout

- *2A share buyback of up to ¥100.0bn was approved at Board of Directors meeting on May 15, 2025 (based on outlook for capital adequacy and cash position)

- *3“Annual dividend per share” reflects dividends after a 4-for-1 stock split; figures for FY2024 and earlier are adjusted to reflect the split; figures in parentheses indicate pre-split dividends (actuals through FY2024; converted amount for FY2025)

Capital policy to achieve our Vision for FY2030

Our Vision for FY2030 is to be a leader shaping the future of the Japanese insurance industry and a global top-tier insurance group. With this in mind, we formulated our current three-year mid-term plan by backcasting from that Vision, which targets market capitalization of ¥6tn in FY2026 and ¥10tn in FY2030.

At the end of FY2024, our adjusted ROE exceeded 10% for the first time, achieving the mid-term plan's final-year target ahead of schedule. As previously mentioned, global top-tier companies have reached even higher levels of ROE, so we raised our target to 12% or higher for FY2026 and 14% or higher for FY2030. Our adjusted profit in FY2024 also exceeded the mid-term plan's final-year target, prompting us to set a new target of ¥450bn for FY2026. We are also considering raising the ¥600bn amount set as the target to aim for by around FY2030.

During the mid-term plan period, we are placing top priority on achieving capital efficiency that consistently exceeds the cost of capital, and we will emphasize shareholder payouts until adjusted ROE stably surpasses the cost of capital.

Under our next mid-term plan starting from FY2027, we will enter a stage of accelerated growth toward achieving our Vision for FY2030. This stage presumes that capital efficiency has already consistently exceeded the cost of capital. With respect to capital policy, we will shift our focus to strengthening dividend payments. At the same time, we will flexibly conduct share buybacks, taking into account the balance between capital efficiency and growth investment opportunities. By pursuing strategic investments and other initiatives, we will also pursue further profit growth and enhance our corporate value.

Through dialogue with stakeholders to reduce volatility and strengthen our management foundation

Engaging with stakeholders to enhance corporate value

We use a variety of opportunities to engage in constructive communication with stakeholders. Feedback we receive is widely reported and shared within the Company, including the Board of Directors and the Executive Management Board, and incorporated into management improvements to help enhance corporate value.

Specifically, we hold quarterly financial results conference calls and semi-annual financial analyst meetings, mainly online, to provide domestic and overseas shareholders and investors with opportunities to learn about our long-term vision and financial results.

In addition, outside directors and group heads participate in theme-specific briefings to explain our business strategies and governance initiatives. Through these efforts, we seek to provide analysts and investors with a clear understanding of our strategies and expand opportunities for them to gain an insight into our initiatives.

In FY2024, we held meetings with more than 200 shareholders and investors in Japan and overseas. We also created opportunities for the Group CEO and Group CFO to visit overseas investors and hear their views firsthand.

In addition to external stakeholders, we host twice-yearly sessions where the Group CFO explains our strategy and financial results to management-level employees. These sessions serve as opportunities to align management and division leaders, thereby strengthening the Group's strategy execution capability. At the briefing on our FY2024 full-year results, we received many questions from employees, and with each session we sense a growing interest among employees in the Company's management.

In FY2024, we introduced a stock-based compensation plan for all employees to foster awareness of corporate value enhancement and align their interests with those of shareholders. Our aim is to accelerate company-wide value creation by helping employees appreciate the benefit of profit sharing when our performance improves. At the aforementioned briefing on our FY2024 full-year results, the Group CHRO joined the Group CFO to explain how performance links to compensation, providing context to foster greater employee interest in management.

We will continue emphasizing highly transparent and reliable disclosure, and through ongoing dialogue with a wide range of stakeholders, we will work to achieve sustainable enhancement of corporate value.

- Financial results conference calls and financial analyst meetings held: 7 times

- Viewers of media broadcasts for individual investors: ca. 100,000

- Number of IR meetings (domestic and overseas): ca. 300